GitHub Copilot Pricing Change: Why Teams Are Switching to Claude

GitHub Copilot shifts from a flat $19 per user monthly fee to usage based billing on June 1, 2026, meaning costs now scale with actual consumption rather than seat count. Enterprises that distributed licences without driving adoption will face unpredictable invoices, forcing a genuine reckoning with whether Copilot delivers enough value to justify continued investment versus alternatives like Claude.

Meta description: GitHub Copilot moves to usage-based billing on June 1, 2026. Here is what changed, why distribution masked a product quality problem for years, the data showing enterprises switching to Claude and OpenAI, and what engineering leaders need to do right now.

1. What is actually changing with GitHub Copilot pricing on June 1, 2026

For the past couple of years, GitHub Copilot at nineteen dollars per user per month was the perfect enterprise AI checkbox. Budget approved, audit question answered, slide deck updated, we use AI. The problem with a checkbox is that it does not ask what you actually did with the thing you checked, and for most organisations the honest answer was that they did not do very much at all beyond distribute the licence and wait for productivity to improve by proximity.

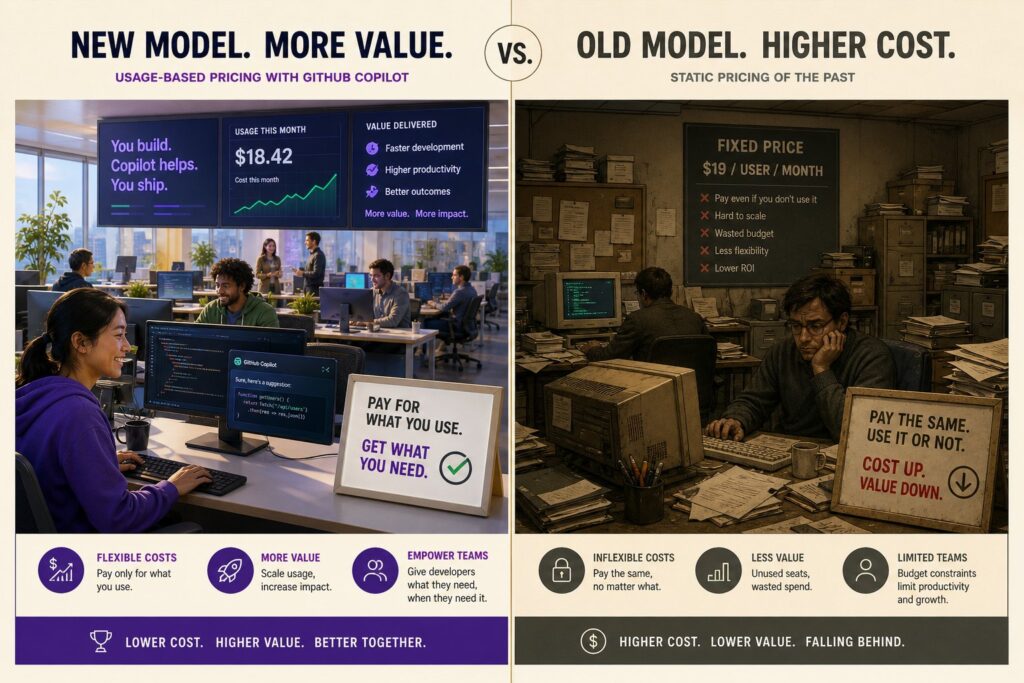

All of that changes on June 1, 2026, when GitHub has announced that all Copilot plans will transition to usage-based billing, converting the monthly seat fee into a pool of GitHub AI Credits consumed by token usage, where one AI Credit equals $0.01. Code completions remain unlimited, but everything else including agents, chat, code review and agentic sessions draws down that pool, and when it is gone it is gone with no rollover. One developer in the community thread estimated that a single agentic coding session routinely consumes between $30 and $40 in credits, which means a Copilot Pro user on $10 per month hits their ceiling in a single working session. The community announcement thread generated more than 400 comments and nearly 900 downvotes, which tells you something about how developers are feeling about discovering, for the first time, what their actual usage costs.

2. Why GitHub Copilot’s flat-rate pricing was always going to end

Microsoft did not price Copilot at nineteen dollars because that reflected the cost of running frontier models at enterprise scale. They priced it there because the goal was adoption, and every seat was a developer habituated to AI assisted coding inside Microsoft’s toolchain, generating Azure consumption, deepening enterprise agreements, and making the case to procurement that the OpenAI bet was paying off.

That bet was enormous enough to restructure the economics of the entire product line. Microsoft has invested $13 billion in OpenAI, with internal planning documents targeting a $92 billion return on that position. OpenAI agreed to pay Microsoft 20 percent of total revenue through 2032 under the renegotiated partnership, with projected payments of more than $13 billion across 2026 and 2027 alone, and Microsoft’s own SEC filings show the OpenAI investment created a $3.1 billion drag on net income in Q1 of fiscal year 2026 alone compared to $523 million the same period the prior year. When the numbers are this large, the question of whether your developer tooling is priced to acquire customers or to generate returns has a fairly obvious answer. Subsidised adoption was always phase one, monetisation is phase two, and phase two started on June 1.

None of this is a betrayal; it is a business model executing exactly as designed, and the mistake was treating a customer acquisition price as a stable infrastructure cost.

3. The flat-rate AI pricing problem: why all-you-can-eat was always a Pizza Hut model

Fixed cost all you can eat pricing for AI consumption is structurally unstable, and it has always been structurally unstable. When you decouple cost from consumption you are relying on one of three things being true simultaneously: either the product is not good enough for anyone to genuinely over-indulge, or the margin structure and supply and demand economics can absorb the outliers without destroying the unit economics of the whole, or there will eventually be a day of reckoning when the vendor has embedded deeply enough into irreplaceable workflows that the price can finally reflect reality.

GitHub Copilot at nineteen dollars was all three of those things at once for most of its life, and then the third condition matured. The product got good enough to over-indulge, the outliers became expensive, the embedding was complete, and the reckoning arrived on schedule. This is the same dynamic that plays out every time a technology platform prices for adoption and then reprices for monetisation, and the sequence is predictable even when its timing is not.

Usage-based pricing is not punitive but honest. Platforms like Claude price by consumption precisely because the alternative requires someone to be wrong about usage at scale. Usage-based billing connects cost to value in a way that flat rate pricing structurally cannot, because flat rate pricing only works when the vendor believes you will not actually use what you are paying for, or has decided to absorb the loss long enough to make switching prohibitive. Neither of those is a foundation for a sustainable enterprise AI strategy, and as soon as the product becomes genuinely useful, the Pizza Hut model breaks, the buffet closes, and the bill arrives.

4. Distribution is not the same as product quality, and the data now proves it

Here is the uncomfortable truth that the nineteen dollar price point obscured for three years. Microsoft’s AI advantage was never a model advantage but a distribution advantage, and those are very different things. Microsoft’s own internal constraints tell the story: its partnership with OpenAI prohibited it from training models beyond a certain size, limiting it to small language models, and the first general purpose language model it tested publicly, MAI-1, ranked well down the performance leaderboards and was never widely released. Microsoft won the procurement conversation, not the engineering one.

The retention data makes the distinction between distribution and product quality concrete. Seventy percent of users initially preferred Copilot because it sits right inside the Office apps they already use, but after trying alternatives only 8 percent kept choosing it. That is not a pricing problem or a discoverability problem but a product problem with distribution masking it entirely, and when users get genuine choice, they leave. Microsoft Copilot’s paid subscriber share dropped from 18.8 percent to 11.5 percent between July 2025 and January 2026, a 39 percent contraction in six months while Microsoft was actively investing in enterprise distribution and deepening its GitHub and Azure relationships. Against a captive base of 450 million Microsoft 365 commercial subscribers, Copilot had converted only 15 million to paid seats after two years on the market, a 3.3 percent penetration rate that represents the industry’s largest AI marketing investment producing less than one in thirty conversions on an audience Microsoft already owned.

SemiAnalysis captured the dynamic in a single sentence in February 2026: Claude for Excel effectively is what Copilot for Excel should have been, but it was launched by an external party on Microsoft’s own first-party application. An outside competitor shipped a better AI experience on Microsoft’s own product than Microsoft’s thirty dollar per seat per month flagship could deliver.

5. Is GitHub Copilot actually good enough at enterprise pricing? How it compares to Claude and alternatives

The pricing reset forces the quality question into the open in a way that subsidised flat rate pricing never did. GitHub Copilot is built primarily on GPT-4o, and GPT-4o is not the best coding model available, and the gap to the alternatives has widened considerably since Copilot achieved its market position.

On SWE-bench Verified, the closest thing the industry has to a standardised real-world coding evaluation testing models against actual GitHub issues from production codebases rather than toy problems, GPT-4o scores 33.2 percent against Claude 4 at 72 to 80 percent depending on the variant, a gap that represents not a marginal difference but a different category of capability on the tasks that senior engineers actually care about: multi-file reasoning, architectural understanding, and complex debugging across large codebases. Among developers who reported using both Claude Code and GitHub Copilot, 61 percent rated Claude Code as more accurate for complex debugging and refactoring, while 73 percent rated Copilot as faster for routine code completion. One tool saves keystrokes while the other eliminates entire development cycles, and at enterprise pricing that distinction is no longer academic.

The developer preference data is striking in its lopsidedness. A JetBrains April 2026 survey scored Claude Code at 46 percent most-loved among developers, compared to Cursor at 19 percent and Copilot at just 9 percent, and most significantly, when JetBrains asked developers with more than ten years of professional experience which tool they would choose for daily work, 46 percent picked Claude Code and 9 percent picked Copilot, a five to one preference ratio among precisely the engineers whose opinions shape what the rest of the organisation eventually adopts.

The trust damage has compounded the quality problem. In March 2026, Copilot injected promotional tips into over 1.5 million pull requests, eroding developer confidence in the platform at exactly the moment the pricing reset was being announced. This is not a footnote but a signal about what happens to product integrity when the monetisation phase arrives and the incentives of vendor and user start to diverge.

6. The numbers behind the switch: where developers and enterprises are actually going

The migration is measurable and it is accelerating. The AI coding tools market hit $12.8 billion in 2026, more than double the $5.1 billion in 2024, and more than half of all code on GitHub is now AI-generated or AI-assisted. This is a foundational infrastructure category in full redistribution, and the redistribution is flowing away from Copilot toward Claude for code and toward OpenAI for everything else.

Copilot’s share of the market measured by developer usage has dropped from 67 percent to 51 percent in the Stack Overflow Developer Survey 2026, and where that share is going is not ambiguous. Claude Code grew from 3 percent to 18 percent at-work adoption between April 2025 and January 2026, a sixfold increase in nine months that no developer tool had previously achieved at that speed, and hit $1 billion in annualised revenue within six months of launch before reaching $2.5 billion by February 2026 with enterprise subscriptions quadrupling since the start of the year. Anthropic’s overall revenue run rate hit $30 billion by early April 2026, nearly triple the $9 billion at end of 2025.

On the non-code productivity side, covering business cases, images, document drafting and general knowledge work, the migration is toward OpenAI rather than Copilot. In paid AI subscriber share, Microsoft Copilot now holds third place at 11.5 percent, trailing ChatGPT at 55.2 percent and Gemini at 15.7 percent as of January 2026, and ChatGPT’s user base has reached 900 million while Copilot usage flatlined at approximately 20 million weekly active users despite a major 2025 upgrade specifically designed to restart growth.

The migration pattern by company size is particularly telling for enterprise AI leaders. Small and mid-size companies now show 75 percent Claude Code adoption, while large enterprises with over 10,000 employees show 56 percent Copilot adoption with Claude Code trailing. The enterprise number is not a product preference signal but a procurement inertia signal, because enterprise contracts, existing GitHub relationships, Microsoft 365 bundles, and SSO integrations keep Copilot in place at large organisations even when the engineers using it would choose something else. The question for enterprise technology leaders is how long procurement inertia can outlast product preference data this lopsided.

The most vivid evidence of where developer preference actually sits came from inside Microsoft itself. In December 2025, Microsoft gave thousands of its own engineers access to Claude Code to compare it head-to-head with GitHub Copilot CLI, and Claude Code became so popular it was described internally as “perhaps a little too popular,” with engineers choosing Anthropic’s tool over Microsoft’s own product while Copilot CLI was quietly ignored. Microsoft wound down the experiment by June 30, 2026, moving engineers back to Copilot CLI not because Claude Code lost the comparison, but because it won it too decisively for the optics to be comfortable. Microsoft’s own engineers voted with their workflows, and the vote was not close.

7. The enterprise AI vendor dependency trap that GitHub Copilot exposed

The organisations now facing difficult CFO conversations are not there because Microsoft changed its pricing. They are there because they allowed a single vendor to become their entire AI layer without building any abstraction between that vendor and their engineering teams, and the pricing reset is simply the moment when the cost of that decision became visible on an invoice.

When your AI strategy is a seat licence, your AI strategy belongs to whoever controls the seat licence. The prompts, the context, the evaluation criteria, and the cost structure all sit on someone else’s pricing roadmap, and AI in the cloud is not aligned with you but with the company that owns it. That is not a sinister observation but a business model description with consequences the moment the incentives of both parties diverge. Studies have found vulnerable code in up to 29 percent of Copilot-generated Python, which compounds the governance problem, because an AI layer you do not own is also an AI layer you cannot fully audit, evaluate, or route around when the quality or risk profile does not meet your requirements. When Microsoft reversed Copilot Chat access in M365 apps in March 2026, analysts noted the move may lead organisations to investigate ChatGPT Enterprise, Anthropic Claude, and Gemini in Google Workspace, with the gap in pricing described as very significant. Each of these reversals is a reminder that the roadmap belongs to the vendor, not the customer.

The engineering teams that are not in that CFO meeting today are the ones that used the subsidised window to build something underneath the licence: their own harness, their own model routing, token budgets, evaluation gates and a layer of abstraction that means when any single vendor’s pricing moves, they have options rather than exposure.

8. Microsoft, OpenAI, AWS Bedrock, and who actually won the enterprise AI infrastructure war

There is a broader context worth naming. Microsoft made an enormous bet on OpenAI as its AI differentiation play, but the OpenAI relationship has simultaneously become the source of Microsoft’s strategic exposure. The cloud exclusivity clause that had bound OpenAI to Azure was formally dismantled on April 27, 2026, meaning the model Microsoft used as its primary AI differentiator is now available through its largest cloud competitor.

OpenAI itself has designated AWS Bedrock as a critical distribution channel, with Amazon investing up to $50 billion and Bedrock becoming the exclusive third-party cloud distribution partner for OpenAI models. When the world’s most valuable AI startup describes a Microsoft competitor as its preferred enterprise distribution mechanism, the strategic picture becomes clear enough that it does not require much interpretation.

AWS has been building a structurally different proposition all along: not a single model bet but a marketplace of models where enterprises access Anthropic, Meta, Mistral, and now OpenAI through a unified platform with consistent governance, IAM integration, and the ability to switch models with minimal code changes. Azure AI’s strategy is tightly coupled to OpenAI’s release cycle, which means when OpenAI experiences instability, Azure AI workloads can be affected. The trade-off is dependency, and that dependency is now visible in pricing, product quality, and market share data simultaneously.

The organisations that abstracted their AI layer early are discovering they have genuine optionality across the entire model landscape, while the ones that treated the seat licence as the strategy are discovering they have a renewal negotiation instead, at the exact moment when the alternatives have never been more compelling or the data supporting them more abundant.

9. What engineering leaders need to do right now before GitHub Copilot costs spiral

Stop the bleeding before the diagnosis. Audit what your agents are actually doing and whether any of it genuinely requires frontier model quality or whether a smaller, faster, cheaper model would produce identical outcomes for that specific task. Agents consuming frontier tokens to generate preambles and pleasantries are not an AI problem but a governance problem with an AI cost centre attached, and the fix is configuration discipline rather than budget escalation.

Establish model routing, because different tasks have different quality requirements and very different cost profiles. A model that costs five times more per token is not five times better for every task but better for the narrow class of tasks where the reasoning gap actually matters, and comparable or worse on everything else. Build the routing layer, measure the quality delta per task class, and stop paying frontier rates for work that does not need frontier capability.

Running a proper evaluation before renewing is now non-negotiable. The pricing reset is an involuntary forcing function to do what should have been done from the start: compare what you are paying against what you are getting, measured against alternatives that did not exist when you originally signed the contract. The developer preference data, the benchmark data, and the retention data all point in the same direction, and the evaluation should too.

Then treat this moment as the opportunity it actually is. Build the abstraction layer, establish evaluation criteria that connect model consumption to actual business outcomes rather than seat counts and licence utilisation reports, and define what AI is supposed to accomplish in your organisation beyond the checkbox on the board deck. Make sure the cost structure you are building reflects a genuine connection between what you spend and what you get, because disconnected consumption models always restore to equilibrium, and the only question is whether you are the one in control when they do.

The era of cheap enterprise AI coding has ended and the era where the real cost structure forces organisations to think clearly about what they are buying has begun, which is ultimately a better place to be even if the CFO therapy required to get there is expensive, because the lesson it teaches is not.

Tags: GitHub Copilot pricing, enterprise AI costs, GitHub Copilot June 2026, AI usage-based billing, GitHub Copilot alternatives, Claude vs Copilot, Claude Code, enterprise AI strategy, AWS Bedrock, AI vendor lock-in, developer tools 2026, Microsoft Copilot market share

References: GitHub Copilot usage-based billing announcement · Enterprise DNA pricing breakdown · Microsoft OpenAI investment · Bloomberg: Microsoft targeted $92B return · OpenAI revenue and Microsoft revenue share · Microsoft SEC filing: OpenAI investment impact · Fortune: Microsoft lost its way in the AI race · Microsoft Copilot 3.3% penetration problem · Microsoft Copilot market share contraction · Microsoft AI numbers: the good, bad and ugly · SWE-bench coding benchmarks explained · Claude vs GPT-4o on SWE-bench · Claude Code vs Copilot head to head · JetBrains developer preference survey 2026 · Copilot PR ads controversy · Claude Code statistics 2026 · Anthropic $30B revenue run rate · Anthropic enterprise revenue growth · Cursor $2B ARR fastest SaaS in history · AI coding market $12.8B 2026 · Microsoft internal Claude Code cancellation · Microsoft engineers preferred Claude Code · Copilot paid subscriber market share third place · Microsoft backtracks on Copilot Chat access · OpenAI Azure exclusivity ends April 2026 · OpenAI AWS Bedrock distribution agreement · AWS Bedrock vs Azure AI comparison · AWS Bedrock multi-model strategy · Copilot code vulnerability statistics · IT Pro: GitHub Copilot billing explained